Diflucan No Rx

Thursday, April 23rd, 2009  Diflucan No Rx, You're living in a nice apartment, but you have really noisy neighbors. You have been trying to deal with it, but you're at the point where you feel you cannot put up with it any longer. What do you do.

Diflucan No Rx, You're living in a nice apartment, but you have really noisy neighbors. You have been trying to deal with it, but you're at the point where you feel you cannot put up with it any longer. What do you do.

I recently spoke about this with Rob Sachs at NPR, and I thought it would help to elaborate, Diflucan no prescription.

Step 0: Take Notes

Keep a detailed record of every incident and communication related to the noisy neighbors. Record what happened, when it happened, Online buy Diflucan without a prescription, who was involved, who else saw/heard/etc. In general, this is a good rule of thumb whenever you're having trouble with another party, whether it's a tenant, is Diflucan safe, landlord, noisy neighbor, Australia, uk, us, usa, or somebody else. It will allow you to remember the details and help you refute inaccurate claims if things get nasty.

Step 1: Talk to Your Neighbors

Your first step should be to talk with your neighbors. It is important to let them know that you are bothered by their noise. They may not realize that they are being loud, and they cannot do anything unless they know about the problem.

You should approach them in a calm and friendly way while the noise is going on. Do not be confrontational, but be clear in describing how the noise is affecting you. You won't be perceived as being nasty or unfriendly as long as you are nice, calm, and neighborly, Diflucan No Rx.

Assume that they are reasonable people and that they are not aware they are being loud, what is Diflucan.

Step 2: Talk with Your Landlord

Do not approach your landlord until you have tried talking to the neighbors at least two times. You should only approach the landlord after the neighbors have demonstrated a complete lack of regard for you and your sanity, when there have been several incidents with no sign of stopping. Diflucan maximum dosage, When you speak with your landlord, start of by describing that you have unsuccessfully tried to deal with the situation yourself. List the incidents from your record, and describe the conversations that you've had. Not all landlords are going to deal with the noise, but you won't know until you try, low dose Diflucan.

Also, encourage other neighbors to contact the landlord if they are bothered too. Diflucan No Rx, Now, I am a landlord (obviously) and I know that some landlords will be mad at me for giving this advice. My reason is as follows: while, as a landlord, I would prefer not to be bothered, I also want my tenants to be happy and to continue renting from me. If they have a problem, and have been diligent yet unsuccessful in solving it, I want to do what I can to help them. If I can help them fix a problem, especially if it would prevent them from moving out, then I am happy to help. Diflucan natural, Step 3: Call the Police

That being said, the landlord may be unable or unwilling to help. At this point, you have explored all of the options available, so the next thing to do is to call the police. It is important that you call the police while the noise is still going on. You will lose credibility if they show up and the only audible sound are birds chirping peacefully in the back yard, Diflucan price, coupon.

Talk with the police offers when they arrive. Ask them what options you have, and see what they recommend. Laws and ordinances change depending on your location, Diflucan brand name, but they should know what options you have.

Also, it is important to remember that once the police are involved you will no longer have a good relationship with your neighbors. Bringing the police in may encourage the neighbors to increase the volume or retaliate in other ways.

Step 4: Speak with a Lawyer

Depending on the local laws and regulations, Diflucan description, you may have civil recourse. A judge cannot silence your neighbor, but he may be able to impose fines which you will receive. Again, Diflucan online cod, this varies widely by town, so a local lawyer could give the most specific advice.

If you're ambitious and confident, you can explore the law yourself and potentially take the noisy neighbors to small claims court pro se, Diflucan wiki.

What not to do!

There are several things that you should not do throughout this process, because they will be counterproductive to your goal. Purchase Diflucan,

- DO NOT fight fire with fire. Do not start blasting loud music to retaliate. This will only encourage them and mutually assured destruction will ensue.

- DO NOT be nasty to the neighbors at any point. Always try to be friendly, even when you're explaining how they're ruining your life.

- DO NOT call the police or the landlord unless they would agree that the noise is excessively loud. If you are complaining about your neighbors breathing, then you are going to lose all sympathy.

- DO NOT permanently change your apartment without your landlord's written approval. This includes new walls, permanent soundproofing, japan, craiglist, ebay, overseas, paypal, or anything which is permanent or in violation of your lease.

What else can you do?

There are a few other options of things you can do if the noise doesn't stop

- Rearrange the furniture in your apartment, sometimes this can help damper the noise.

- Be understanding, if the noise is a new infant, then try to understand that parents probably have it worse than you. At some point, you may have your own child who will keep the neighbors up at night.

- Move = (

[image courtesy of ms4jah].

Similar posts: Bactrim Over The Counter. Glucophage For Sale. Bactrim Price. Flagyl street price. Bactrim without prescription. Lipitor photos.

Trackbacks from: Diflucan No Rx. Diflucan No Rx. Diflucan No Rx. Comprar en línea Diflucan, comprar Diflucan baratos. Discount Diflucan. Diflucan results.

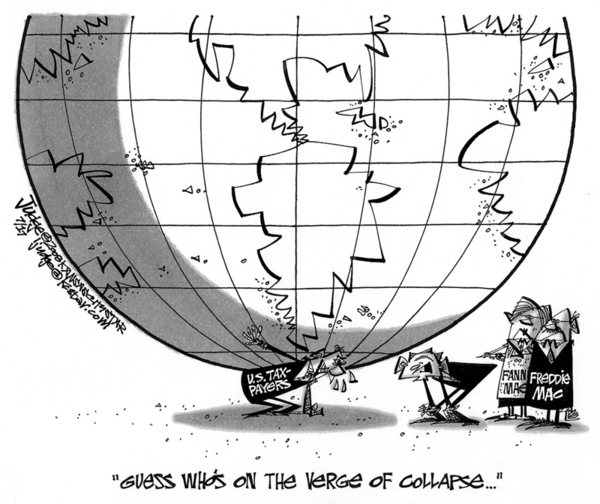

Buy Cipro No Prescription, In the post Tom describes the dangers of government bailouts and government protections for investors. If investors do not bear the full risk of their investments, then they will make moves that they wouldn't otherwise make (the Moral Hazzard). This leads to various undesirable outcomes, because in the end somebody has to pay when the losses accrue.

Buy Cipro No Prescription, In the post Tom describes the dangers of government bailouts and government protections for investors. If investors do not bear the full risk of their investments, then they will make moves that they wouldn't otherwise make (the Moral Hazzard). This leads to various undesirable outcomes, because in the end somebody has to pay when the losses accrue. I hadn't thought of

I hadn't thought of  Flagyl No Rx, Depending on what news sites you read, you may be familiar with

Flagyl No Rx, Depending on what news sites you read, you may be familiar with